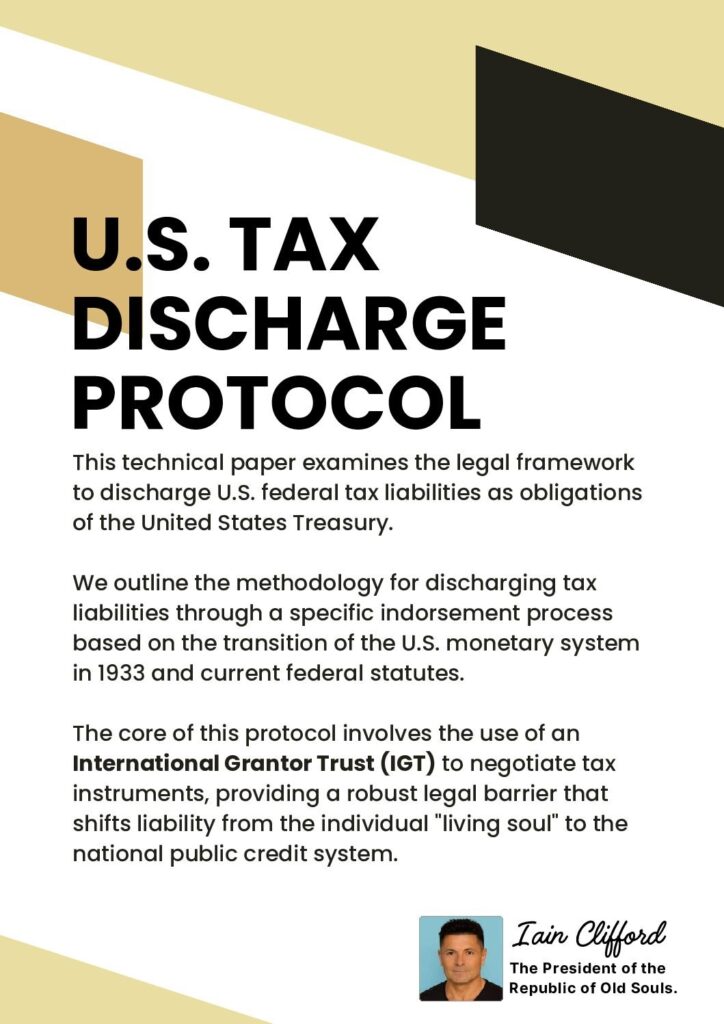

Under federal law, an obligation issued by an authorised officer of the United States qualifies as an obligation of the United States itself.

A federal tax bill meets this definition.

It is not a private debt between two equal parties.

It is an instrument issued by the Treasury system.

This Protocol examines how such instruments may be returned, indorsed, and settled through the same system that issued them.

Federal law defines an “obligation or other security of the United States” to include bills, checks, or drafts for money drawn by or upon authorised officers of the United States.

18 U.S. Code § 8